: Valuation Snapshot as Corporate Governance, Funding Pressures, and Legal Setbacks Collide")

Sable Offshore (SOC) finds itself at the center of a high-stakes moment as several issues converge. Allegations against the CEO, urgent funding needs related to a renewed loan with Exxon Mobil, and board-level investigations are shaping investor attention.

See our latest analysis for Sable Offshore.

Sable Offshore’s share price has been hammered in recent weeks, dropping nearly 63% in the past seven days and down 80% year to date, as the market reacts to news of leadership turmoil, urgent fundraising efforts, and regulatory setbacks. With a one-year total shareholder return of -79.5%, both momentum and investor confidence appear to be fading. This underscores the heightened risk and uncertainty around the stock’s outlook.

If this sort of high-stakes turnaround has you considering what else is out there, now’s a smart time to broaden your perspective and discover fast growing stocks with high insider ownership

Given the scale of recent losses and the sharp discount to analyst price targets, the key question now is whether Sable Offshore’s dramatic selloff represents a genuine buying opportunity, or if the market is already reflecting future risks and growth in the current price.

Price-to-Book of 1.3x: Is it justified?

With Sable Offshore trading at a price-to-book ratio of 1.3x and its last close at $4.84, investors are seeing a valuation exactly in line with the US Oil and Gas industry average.

The price-to-book ratio is commonly used to assess how the market values a company’s net assets, especially in asset-heavy sectors like oil and gas. At 1.3x, Sable Offshore appears to be valued similarly to its industry peers, suggesting the market is pricing in no premium for its future prospects or current stresses.

Compared to the rest of the industry, Sable Offshore’s price-to-book stands right at the sector average and does not command a discount or premium. Notably, when measured against peer averages, its ratio appears far lower than some outliers in the space. The market is signaling that, despite the recent sharp share price decline, Sable Offshore’s asset value is not being viewed as fundamentally worse than the broader peer group.

See what the numbers say about this price — find out in our valuation breakdown.

Result: Price-to-Book of 1.3x (ABOUT RIGHT)

However, significant net losses and ongoing leadership instability could hinder a near-term recovery. These factors may keep sentiment under pressure despite the recent valuation reset.

Find out about the key risks to this Sable Offshore narrative.

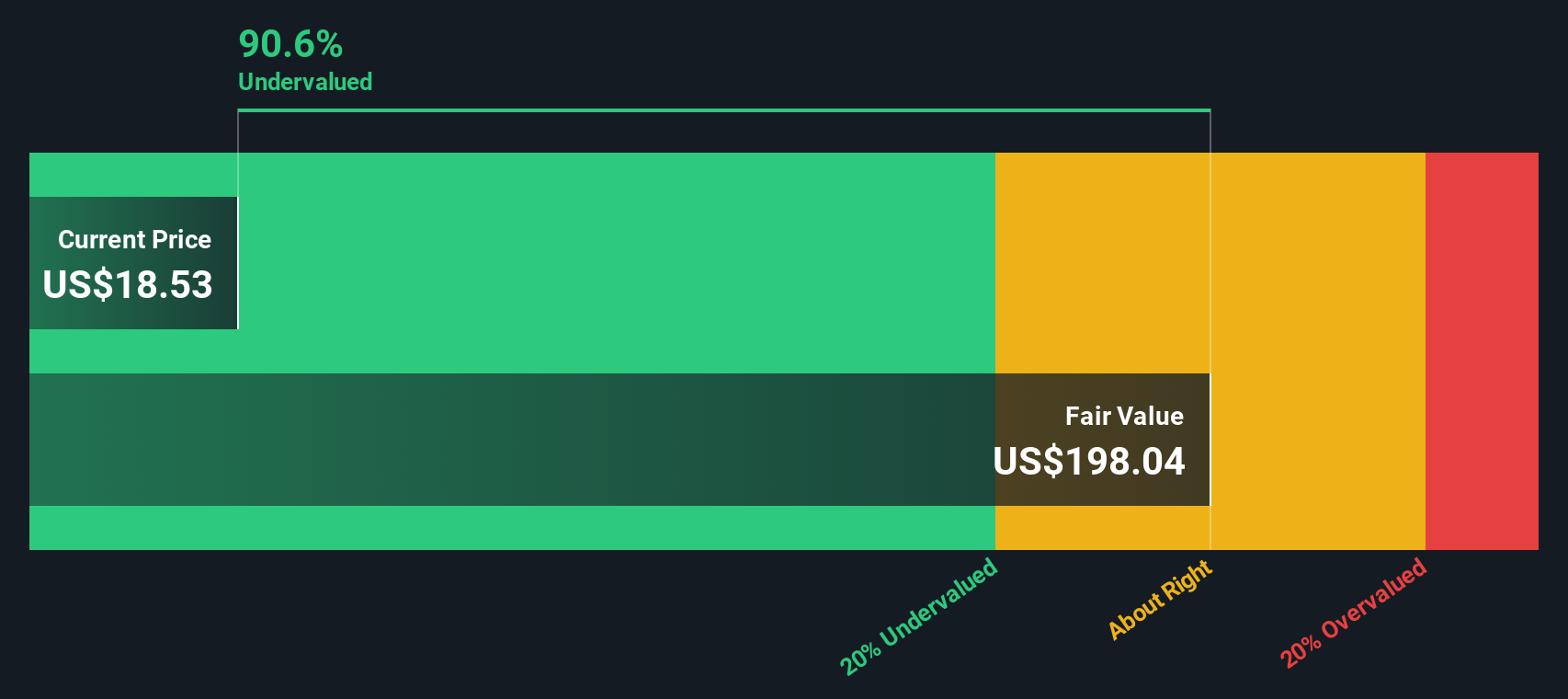

Another View: Discounted Cash Flow Tells a Different Story

While the price-to-book ratio puts Sable Offshore in line with its industry peers, our DCF model suggests a vastly different valuation. Sable is trading at a steep 96.5% discount to what our DCF calculates as fair value. This implies the market might be overlooking its future cash flow potential. Could this disconnect signal a hidden opportunity, or is it a sign of investor caution for good reason?

Look into how the SWS DCF model arrives at its fair value.

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out Sable Offshore for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 845 undervalued stocks based on their cash flows. If you save a screener we even alert you when new companies match – so you never miss a potential opportunity.

Build Your Own Sable Offshore Narrative

If you see the story differently or want to dig deeper into the figures, it’s quick and easy to shape your own perspective in just a few minutes. Do it your way

A great starting point for your Sable Offshore research is our analysis highlighting 2 key rewards and 4 important warning signs that could impact your investment decision.

Looking for More Investment Ideas?

Make your next move count by checking out stocks with exceptional growth potential, robust dividends, and exposure to the forefront of quantum innovation. Don’t let opportunity pass you by. Your smartest investments could be just a click away.

This article by Simply Wall St is general in nature. We provide commentary based on historical data

and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your

financial situation. We aim to bring you long-term focused analysis driven by fundamental data.

Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

Simply Wall St has no position in any stocks mentioned.

New: Manage All Your Stock Portfolios in One Place

We’ve created the ultimate portfolio companion for stock investors, and it’s free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Try a Demo Portfolio for Free

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

link