The Securities Commission Malaysia (“SC”) seeks public feedback on the proposals set out in the Discussion Paper: Corporate Governance Framework – Strengthening Governance Practices and Driving Behavioural Shifts for Sustainable Value Creation (“Discussion Paper”) published on 12 December 2025, as part of its review of Malaysia’s corporate governance framework.

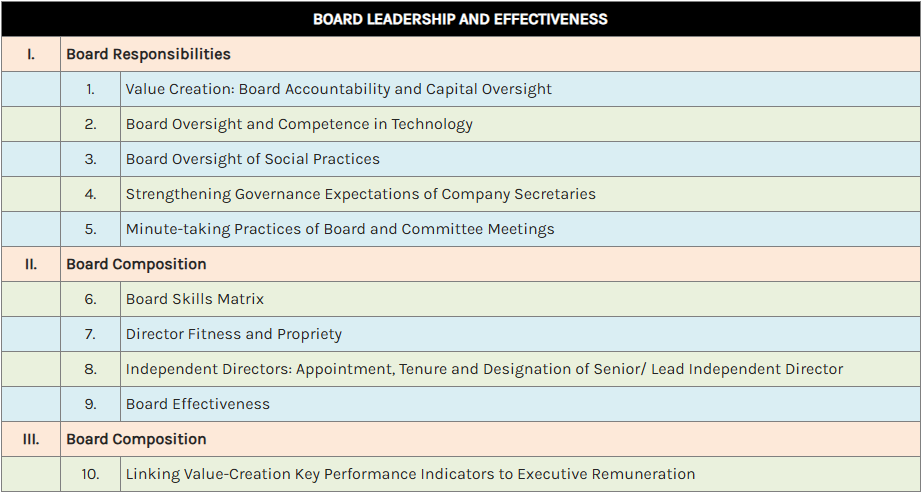

The proposals are set out under three key principles, namely Board Leadership and Effectiveness, Effective Audit and Risk Management, and Integrity in Corporate Reporting and Meaningful Relationship with Stakeholders, which are divided into seven themes and 17 specific topics. Broadly, the framework of the Discussion Paper is as follows:

The Discussion Paper sets out 55 proposals for which feedback is sought by the SC, as well as a general question that allows a respondent to put forward any suggestion which could improve practices and conduct to strengthen the corporate governance framework in Corporate Malaysia.

Some of the proposals under the themes described below are as follows:

Value Creation: Board Accountability and Capital Oversight

1. Should boards be expected to place greater emphasis on overseeing long-term value creation and capital discipline, including capital management, capital allocation, and monitoring of post-investment outcomes?

2. Should companies be mandated to disclose and articulate how their purpose, values and strategies collectively contribute to long-term value creation?

3. What measures, incentives or programmes would best support boards and management in prioritising long-term value creation?

Board Oversight and Competency in Technology

4. Should there be a distinction or difference in expectation for boards across various industries, such as higher expectations for boards in digital-intensive sector (as compared to other sectors) vis-à-vis utilisation of technology, governance structure in managing technology, and competencies including AI or data-governance experience, whether in board composition or external advisory arrangements?

Strengthening Governance Expectations of Company Secretaries

5. Should the role of company secretaries as ‘governance gatekeepers’ be strengthened?

Board Skills Matrix

6. Should boards (through the Nomination/ Nominating Committee (“NC”)) be expected to maintain a company specific, strategy-linked skills matrix?

7. Should the skills matrix be publicly disclosed in the annual report or Corporate Governance Report, or serve as an internal document to guide the NC?

Director Fitness and Propriety

8. Should clearer expectations on the content of Fit & Proper policies be set?

9. What exclusionary or high-risk factors should be included in Fit & Proper policies (e.g. ongoing criminal proceedings)?

10. Should a limit on concurrent executive directorships be introduced, particularly for the roles of Chief Executive Officers, Managing Directors and Executive Chairs? If so, how should the limit be framed?

Independent Directors: Appointment, Tenure and Designation of Senior/Lead Independent Director

11. Should the two-tier voting mechanism be made mandatory for the reappointment of Independent Non-Executive Directors (“INEDs”) beyond nine years (up to the 12-year cumulative term limit)?

12. Should the tenure of INEDs be limited to a cumulative term of nine years, instead of the current 12-year limit?

13. Should NCs be required to disclose, at a minimum, the rationale for the appointment of INEDs, including how the candidate meets the company’s needs, the basis for independence and time commitment?

14. Should large Public Listed Companies (“PLCs”) and those with a Non-Independent Chairman be required to designate a Senior Independent Director or Lead INED?

Board Effectiveness

15. Should the NC’s decisions on board appointments give greater consideration to age diversity within the context of an outcomes-based approach?

16. Should boards disclose how their composition, including age profile and succession planning, supports continuity, renewal and alignment with the company’s strategic objectives?

17. Should Malaysia move towards mandatory quotas (e.g. for gender diversity) to accelerate change, or continue promoting voluntary adoption and market-driven incentives?

18. At a minimum, should the disclosure of the outcomes of board effectiveness evaluation cover the following:

- whether the evaluation was conducted internally or by an external independent party;

- the scope of the evaluation;

- the criteria used; and

- the outcome of the evaluation, including actions taken to address recommendations.

Linking Value-Creation Key Performance Indicators to Executive Remuneration

19. Should long-term value creation indicators be linked with executive remuneration?

20. Should the linkage of value-creation indicators to executive remuneration apply to all PLCs, or to specific groups (for example, large PLCs)?

21. What challenges may companies face in linking value-creation indicators such as Relative Total Shareholder Return (TSR) and Return on Equity (ROE) to executive remuneration, and in disclosing this linkage?

Enhanced Disclosure in the Appointment and Reappointment of External Auditors

22. What are a respondent’s views on the proposal to introduce enhanced disclosure requirements for the appointment and reappointment of external auditors?

Tendering of Audit Firms

23. What are a respondent’s views on the proposal to recommend companies to conduct re-tendering of the current audit firms that have serviced the company for more than 10 years?

24. Does a respondent agree with the proposed timeline to carry out the audit tender i.e. within three years after the 10-year period served by the incumbent external auditor?

Risk Management Committee

25. Should all PLCs be expected to establish a dedicated Risk Management Committee?

Competency of Internal Auditors in Emerging Areas

26. Should internal auditors play a stronger role in supporting the board and management in assessing the effectiveness of the company’s governance, risk management and internal control systems in relation to emerging areas?

27. To what extent should internal auditors be expected to integrate emerging risks and developments into their audit universe and audit plans?

28. Should the NC be expected to disclose its rationale for recommending a director, referencing the board skills matrix, succession needs and alternatives considered?

29. For reappointments, should the NC be expected to disclose decision-useful information on its assessment, including directors’ time commitment, management of conflicts of interest, fit and proper considerations and how the directors have performed their roles?

According to the SC, the feedback will guide the upcoming revision of the Malaysian Code on Corporate Governance (MCCG), and relevant corporate governance framework, ensuring the framework remains forward-looking, relevant and aligned with global best practices.

Relevant stakeholders including listed companies, directors, company secretaries, investors, professional bodies and industry associations are encouraged to provide feedback on the proposals set out in the Discussion Paper which is to be submitted to the SC by 6 February 2026 through the following:

Comments

The Discussion Paper includes many interesting proposals drawn from the SC’s observations on existing practices in Malaysia as well as the developments in other jurisdictions such as the United Kingdom, Australia, Singapore, Hong Kong, Japan and Korea. The proposals, if adopted, will raise the level of corporate governance practice in Malaysia.

link