U.S. Shareholder Proposals: A Decade in Motion

Shareholder proposals, often seen as a bellwether of investor sentiment and preferences, have gone through a significant shift over the past decade. The number of proposals on environmental and social topics exploded, surpassing the governance and compensation topics that had dominated the discourse in mid-2010s. In recent years, discussions related to environmental, social, and corporate governance (“ESG”) risks have become highly politicized, including attempts to politicize the shareholder proposal process. However, investors show little to no interest in proposals that advocate a political viewpoint without demonstrable economic relevance. ISS-Corporate reviewed the data of shareholder proposals submitted at U.S. companies from July 2014 to June 2024 and examined how shareholder proposals as well as corporate behavior and disclosures on sustainability and corporate governance have changed over the decade.

KEY TAKEAWAYS

- E&S campaigns remain active: Environmental and social topics outnumbered governance and compensation requests over the past four years, with proposals focusing on climate change and human capital management driving the surge in proposals.

- Fewer withdrawals in 2024: The percentage of withdrawn proposals has dropped compared with previous years, indicating that proponents and issuers are finding less common ground through engagement.

- Support levels remain lower but have not dropped further: Support levels fell sharply from the peak in 2020-2022 and then stabilized in 2023 and 2024.

- Anti-ESG campaigns grow in numbers but lack support: Proposals countering environmental and social initiatives make up approximately 11% of the total submitted in 2024, but support levels remain in low single digits. These politicized campaigns have failed to make the case for the economic impact related to the requests.

- Corporates are making improvements: Large-cap firms, which are predominantly the targets of shareholder campaigns, have made great strides in their disclosures and practices in recent years. As proposals seek more ambitious action at these firms, it becomes more difficult to gain broader investor support, partially explaining the drop in overall support levels.

Greater Focus on Environmental and Social Risks

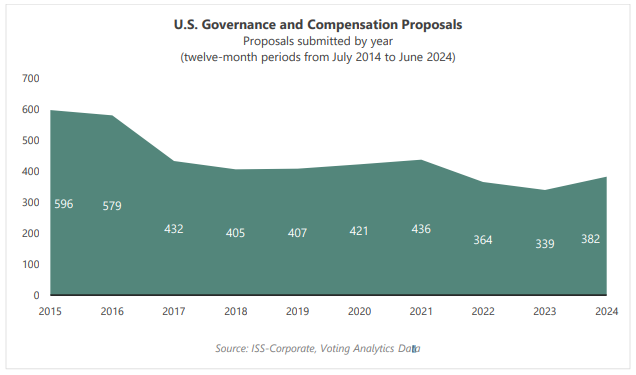

Shareholder proposals related to governance and compensation topics represented the largest portion of proposals up until the mid-2010s, but their volume decreased over the past ten years. Over the decade, many governance-related issues were either resolved or became less prominent, though persistently large volume indicates that governance and compensation remained important, but with fewer new or unresolved issues emerging. The number of governance and compensation proposals slightly rebounded in 2024, indicating renewed concerns about executive compensation and corporate governance issues, possibly triggered by evolving market conditions or shifts in corporate behavior post-pandemic.

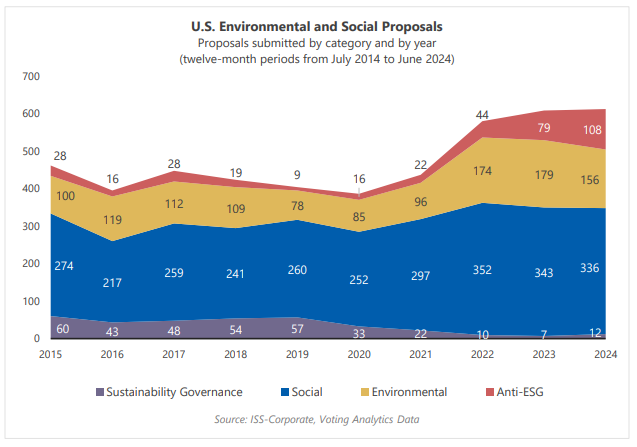

A decline in governance and compensation proposals was replaced by the surge in environmental and social proposals as investors’ focus shifted towards sustainability issues. Proposals related to environmental and social topics accounted for 62% of the total in 2024, up from 44% a decade earlier. In absolute terms, environmental and social proposals increased by 57% from 2020 to 2022 and continued to rise to a record 610 in the 12 months through June 2024. However, the increase in volume in the past two years is primarily due to the higher prevalence of proposals seeking to counter environmental and social initiatives, often referred to as “anti-ESG” proposals, as those requests reached a record number of 108 in the year. The overall surge in submitted proposals observed in 2022 was likely the direct result of the November 2021 SEC Staff Legal Bulletin, which provided updated guidance on procedural requirements for shareholder proposal submissions and made it more difficult for companies to exclude proposals from the ballot.

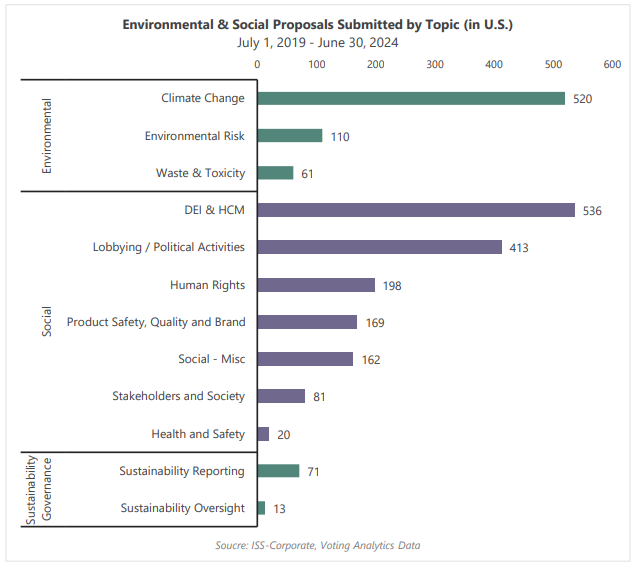

When taking a closer look at the volume of proposals submitted by topic in the five years through June 2024, it becomes apparent that Climate Change and Human Capital Management have driven the increase in environmental and social proposals. Approximately 75% of environment-related proposals submitted during this period focused on climate-related issues, with an increased emphasis on alignment with the Paris Agreement and net zero targets.

Requests related to human capital management cover a wide range of topics, including diversity, inclusion, discrimination in the workplace, employee benefits, and gender and racial pay equity. These proposals outpaced those related to all other social topics, which does not come as a surprise, given the heightened attention employee and racial equity issues received during and in the aftermath of the COVID-19 pandemic. Proposals related to lobbying and political activities remain high on the agenda, especially given the contentious political landscape in the U.S., creating challenges for businesses. Concerns related to human rights and supply chains continue to feature prominently in proponents’ requests, while a wide range of new social topics have surfaced on meeting agendas in recent years, including questions around misinformation in social media and advertising and the use of generative artificial intelligence.

Fewer withdrawals, more proposals going to a vote

The final status of a proposal varies widely after it is submitted to a company. Not all proposals end up on ballots. Some are withdrawn by proponents prior to the meeting, while others may be “omitted” by the company per Rule 14a-8 of the Securities and Exchange Commission (SEC). Proposal withdrawals typically signal some form of settlement between the proponent and the company following direct engagement, often indicating concessions being made between the parties. A higher rate of omissions may indicate less effective proponent campaigns, as the proposals may be deemed to violate the relevant rules established by the SEC (i.e., improper drafting, ordinary business exception, relevance, duplication, resubmission limits, or conflict with company’s proposal). However, omissions rates may also depend on changes in the guidance provided by the SEC, providing stricter or looser requirements related to no-action relief (the SEC’s formal agreement for a proposal to be excluded).

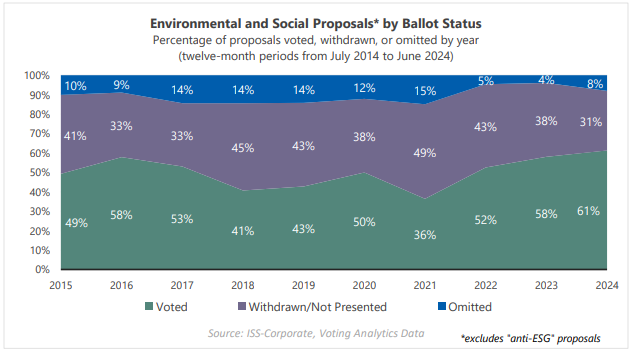

The changing trends in ballot status become pronounced when observing environmental and social proposals. The percentage of withdrawn proposals increased in the 2010s, compared with previous decades, demonstrating greater traction by campaigns focusing on environmental and social issues. In 2021, withdrawals reached a record 49% of all submitted environmental and social proposals, corresponding with record support levels and overall momentum towards greater transparency and commitments in relation to sustainability management. Since 2021, the percentage of withdrawn proposals has steadily declined, reaching 31% of submitted proposals in the year through June 2024. The lower rate of withdrawals of environmental and social proposals suggests companies and proponents are finding less common ground. That may be an outcome of companies making significant efforts to improve sustainability disclosures and management programs over the past five years, while proponents’ requests increasingly push the envelope for more robust disclosure criteria or action plans.

The rate of omissions for environmental and social proposals dropped sharply to 5% in 2022 from 15%. This is likely a direct result of updated guidance by the SEC in November 2021 that made the exclusion of certain shareholder proposals more challenging and also served as a catalyst in the surge of shareholder proposals observed in 2022. That said, omissions related to environmental and social proposals edged upwards in 2024 to 8% of proposals from 4% the year before. As a result, 2024 saw the highest rate of environmental and social proposals going to a vote (61%) in recent years.

This analysis excludes so-called “anti-ESG” requests, which have historically demonstrated much higher rates of omissions and lower rates of withdrawals compared to requests that seek greater transparency and improved management. In the 12 months through June 2024, only 6% of “anti-ESG” proposals were withdrawn and 10% of such requests were omitted in the same period.

By comparison, significantly fewer governance and compensation proposals were settled behind the scenes. Nearly 70% of governance and compensation propsoals went to final vote over the decade, compared to 51% for environmental and social proposals, indicating limited willingness amongst parties to resolve the issue thorugh negotiation and a greater success companies had in blocking governance and compensation proposals. However in 2024, while the overall volume of governance and compensation proposals submitted increased, those that went to vote dropped to 64% and omitted proposals jumped to 23%. The increase in both the proposals submitted and those omitted was due in part to new types of governance proposals being presented, including those seeking to amend director resignation policy, that were often ommitted from the ballot.

Support drivers: a dynamic equation

A review of trends in support levels for proposals that went to a vote can provide insights into investor sentiment on issues presented on ballots as well as other factors. In addition to an evolution of investor perspectives, support levels can serve as indicators of the evolution in the questions raised by proponents as well as the evolution of company practices.

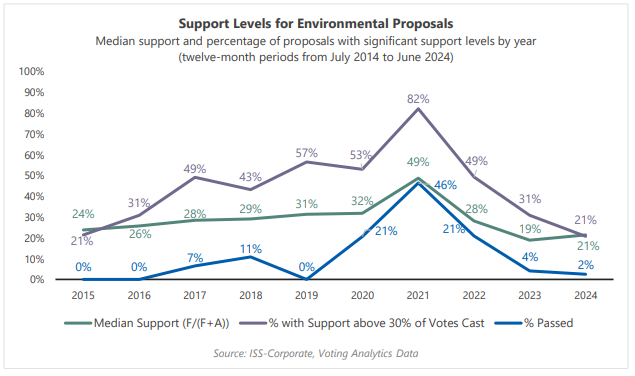

Support level trends for environmental proposals imply a rapid evolution in all these areas. Following a gradual increase in support levels, 2021 saw an explosion in support for environmental proposals (primarily focusing on climate change), with a record number of 46% of voted proposals passing and a median support level of 49% of votes cast. In subsequent years, median support levels plunged to 19% of votes cast in 2023 and 21% in 2024.

The volume of voted environmental proposals remains at historically high levels, with 97 and 82 proposals going to a vote in 2023 and 2024, respectively. However, engagement around these topics is becoming more nuanced, as target companies exhibit more mature environmental management programs and more advanced climate disclosures. Proposals are also becoming more demanding, as most climate requests now ask companies to establish science-based targets or similar commitments, compared with broader requests around climate transition plans a few years ago. As campaigns typically address large-cap companies, proponents may find it more challenging to demonstrate significant gaps in companies’ programs and rally broad support from other investors, since companies are better able to demonstrate progress. At the same time, investors likely show more caution and a more measured approach in their voting practices, especially amidst scrutiny and political pressure from key stakeholders in relation to their ESG efforts.

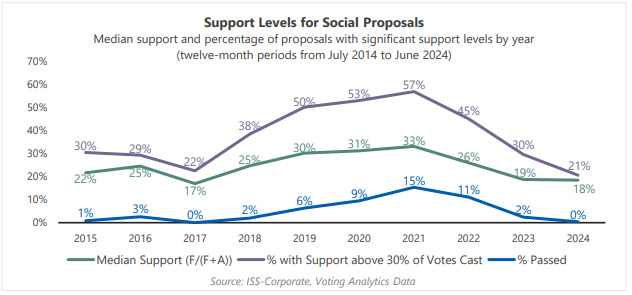

A similar though less pronounced trend can be observed among social shareholder proposals. The median support level on social shareholder proposals gradually increased, peaking in 2021 at 33% of votes cast, and then waned in 2022 and 2023. The same trends discussed in relation to environmental proposals underly voting patterns in social proposals, as improved company disclosures and programs, more rigorous proposal requests, and a more nuanced approach by investors lead to lower support levels for these initiatives. At the same time, the volume of voted proposals dealing with social issues remains at historical highs, demonstrating the continued interest in identifying material risks in relation to these issues by market participants.

The number of governance and compensation proposals voted upon as well as their support level have been relatively stable over the years, though both have trended downward. During the period studied, 2015 saw the highest number of proposals voted, with more than half gaining over 30% of the votes cast and roughly a quarter of them passing. The steady decline in volume and support may not necessarily indicate declining interest among shareholders on governance matters but rather a general improvement in the governance structure of companies. Support dropped notably in 2023, which appears to be driven in part by an increase in compensation-related proposals where there is a greater divergence of opinion among shareholders. The support level rebounded in 2024, pushed by an increase in proposals to eliminate supermajority vote requirements which tend to receive universally strong support from shareholders.

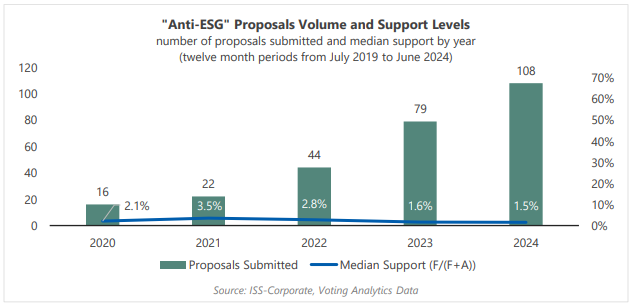

Proposals seeking to challenge, reverse, or counter environmental or social initiatives by companies have seen a dramatic rise in recent years, with so-called “anti-ESG” proposals making up approximately 11% of all requests in the year through June 2024. That’s up from approximately 2% of submitted requests from July 2014 to June 2021. These campaigns are primarily driven by political advocacy groups, including the National Center for Public Policy and Research and the National Legal and Policy Center, which have submitted more than 80% of these proposals in the past three years. Their campaigns cover a wide range of topics, but key themes include challenging company DEI commitments on the grounds of potential reverse discrimination, questioning climate commitments and their associated cost, scrutinizing company’s affiliations, partnerships, and political involvements, and raising concerns related to company operations in China.

Despite the high volume of submitted proposals, support levels for anti-ESG requests remain low, with a median support level of 1.7% of votes cast during the past three years (July 2021 to June 2024). The main reason for the consistent levels of low support pertains to the fact that these requests are presented with a focus on a political agenda. Even requests that have attempted to present an economic argument are generally framed along the lines of a political debate, which tends to dominate over other points raised by proponents. The low support levels observed for these campaigns generally align with historical trends for shareholder proposals that tend to focus on political points or values-based assertions (of any political persuasion) but fail to address the economic impact of the business practice under consideration.

These campaigns serve as a reflection of the highly polarized political landscape in the U.S. as well as misperceptions of sustainability efforts as political statements instead of risk management considerations.

Changes in Corporate Practices Explain Key Trends

Intensifying political debate around ESG topics and declining support on environmental and social proposals do not necessarily indicate a de-prioritization of sustainability. Regardless of political sentiments, companies have been steadily enhancing their practices and disclosures.

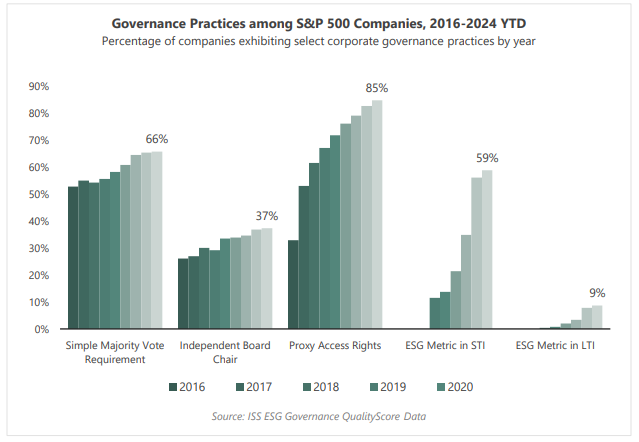

Both the volume and support level of governance and compensation proposals declined since 2015, but there was a consistent and steady enhancement in corporate governance practices. Among S&P 500 companies, which are the target of most shareholder proposals, those granting proxy access rights have increased by more than 50 percentage points, from one-third in 2016 to 85% in 2024. Proxy access rights proposals were the most common and one of the most successful shareholder proposals until 2018, when the volume started to drop following the broad adoption of the practice among S&P 500 companies. Other good governance practices, such as a simple majority vote requirement to amend bylaws or charters and an independent board chair increased as well. In addition, more and more companies are tying a portion of their executive pay with environmental and social considerations, creating economic incentives to improve ESG practices.

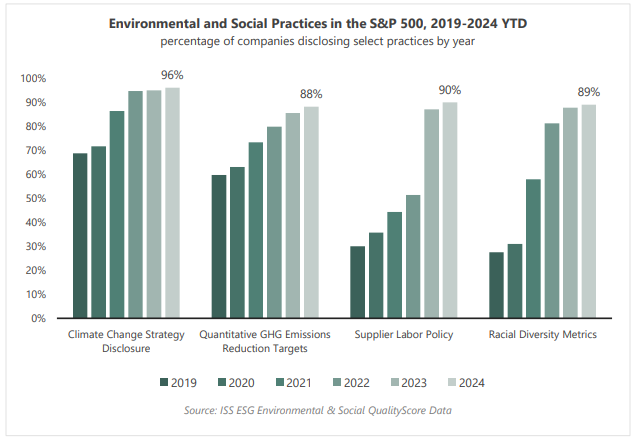

Sustainability disclosures and practices have also evolved considerably in the past five years. The graph below demonstrates the rapid progress. Approximately 96% of companies in the S&P 500 disclose some form of climate change strategy, while 88% have established quantitative GHG emissions reduction targets. Human rights policies, supplier codes of conduct, employee demographics data (by gender, race, and other categories) are widely available and expected. Larger gaps in disclosures are found among mid- and small-capitalization firms. However, the same trends toward greater disclosure are prevalent across companies of all sizes. While there still may be room for improvement at all levels, the significant progress made and the greater level of maturity in disclosures among large-capitalization companies helps explain the drop in support levels for environmental and social proposals. According to ISS-Corporate Voting Analytics data, 82% of shareholder proposals dealing with environmental or social issues were submitted at S&P 500 companies.

Economic Impact Still Matters

Several factors can affect the proposals put forward by shareholders as well as their support level. These include investor sentiment, the type of request submitted, company practices, and broader stakeholder considerations and priorities.

Two factors have remained constant over the decades: 1) the extent to which the investment community recognizes the economic and business relevance of the topic in question and 2) whether companies sufficiently address the associated economic risk. Economic relevance remains the most important determining factor for investor support of shareholder proposals, regardless of whether a proposal is perceived as “progressive” or “conservative.” Over the past decade, proposals that have primarily focused on advocacy efforts and political positions have generally failed to gain broader shareholder support, whereas proposals that have made the case for economic risk or a level of transparency that could help with investment decisions have generally resonated more with investors.

1Shareholder proposal data (and relevant mentions of any specific years throughout this publication) are based on twelve-month periods starting on July 1 of the previous year and ending on June 30 of the reference year.(go back)

link